Spreadsheets are an accountant’s best friend. The flexibility that a spreadsheet offers is fairly compelling and it’s no wonder it’s the first solution that comes to mind when thinking of complex calculations. It is then no surprise that businesses have been looking to spreadsheet solutions for transitioning to the new lease standards. However, the impact of the regulations on lease processes are profound and businesses will need to be aware of the requirements before trying to tackle lease compliance for IFRS 16 & ASC 842 with a spreadsheet solution.

The following are important areas of compliance that businesses will need to consider:

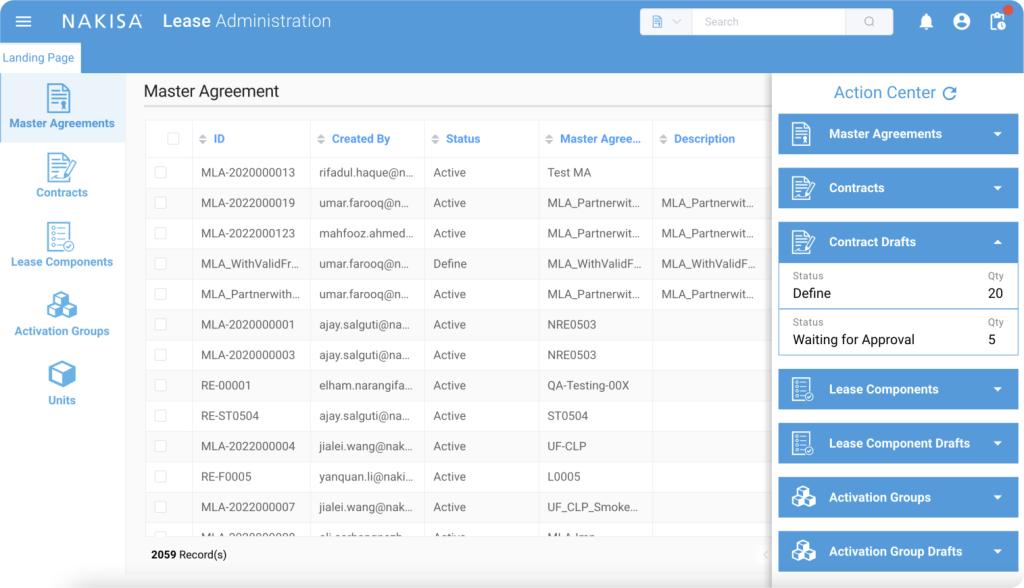

Data Collection and unification

The real challenge lies in centralizing the data so that it will provide adequate visibility into lease portfolio and its exposure to new standards. Data needs to be unified in one single repository so that calculations, judgements, reassessments, transitional accounting, disclosures etc. can be made. Is a spreadsheet a database that is robust enough to comply with these requirements? Well for a start, a spreadsheet is not a database. Yes, it offers rows and columns, but these rows and columns are not suitable for storing a huge volume of information which can be managed effectively across a large organization.

Data validation and traceability

The current reality for many businesses is that a significant portion of their leases data is stored in filing cabinets. The effort that is required to gather missing lease information from hard copies of contracts that are being kept in the filing cabinets is significant. What’s more, how would you make that data trackable so that it can be traced back to the source? Having a sound audit trail is very important for the new lease standard as it requires judgement and constant assessments when there is a modification. Does a spreadsheet offer you an audit trail sufficient for compliance? Does it offer you the approval matrix or workflow that is required for lease classification and modifications? Does it offer you a history of changes or simply the change log? These are the questions that need to be answered by any solution being considered.

Parallel reporting

There would be a need for parallel reporting during the transition to the new standard. The lessee would need to know the overall liability (and asset) balance they currently have under existing leases and what the balance would be when they assess and classify theses leases under the new standard.

For a public company, with a December 31st year-end, that reports three years on financial statements (current year plus two previous years as comparatives), under U.S. GAAP, the effective date will be 1 January 2019 and the transition provisions must be applied beginning 1 January 2017.

Disclosure

The new standard requires extensive list disclosures to be added as notes to the financial statements. While existing systems may include some lease information, they may not have all of the information required to make disclosures necessary to comply with the new standard. As such, significant effort will be required to manually gather missing lease information. As mentioned before, a spreadsheet is not a database which can store all the information required for disclosures.

Lease modification

In the parallel reporting period and beyond, an entity should also look into the changes in the terms and conditions of a contract that result in a change in the scope of or the consideration for a lease. Also, they should look into the effect of changes in the renewal, termination, purchase decisions and in the estimate of guaranteed residual value (GRV) payout, during the parallel reporting period and beyond. Will a spreadsheet suffice to do these ongoing assessments of lease term and the accounting for lease modifications?

The Lost opportunities

Ultimately, a business looking at a spreadsheet solution is missing out on several opportunities.

- Unification: Lease contracts are dispersed across business units and geographic location adding significant work to assemble leasing data.

- Cost Savings: Lack of lease event notifications and casualty tracking means businesses will still be paying significant sums of money for penalties and lost assets.

- Simplified Reporting: Reporting requirements will increase administrative burdens and introduce more opportunities for error.

- Transparency: Auditing transparency will be extremely difficult if not impossible for many businesses.

- Lease Management: Managing leases will continue to be a largely manual process and will contribute to suboptimal lease decisions in addition to the manual workload.

- Collaboration: Individuals responsible for aspects of leasing will need to use other solutions and manual processes in order to coordinate lease accounting and management .

Conclusion

Rather than relying on spreadsheets to do the job, businesses should be looking to solutions that can accelerate & improve compliance and lease management instead of just meeting the standards minimum requirements.

This means finding solutions that integrate with existing financial systems, unify lease data, enable communication and collaboration, automate accounting, enable full lease lifecycle management, and support compliance with IFRS 16 and ASC 842.